What is a personal financial statement? How important is it? What are its benefits, especially for working people or the general public?

When it comes to financial statements or accounting, many people start to lose interest because they think it is too difficult or they may not know what they are doing and do not see the benefits of these things.

There is also a misunderstanding that only business owners need to prepare financial statements because there are many taxes and expenses that need to be paid, which is actually not relevant at all. Ordinary people should do it because if we consider money to be very important, we should know our real financial situation. Is it safe or risky?

What will tell us clearly is the personal financial statement.

Personal financial statement is like an X-ray of our financial health. Personal financial statement will tell us our financial information such as assets, liabilities, income, expenses or items related to money. Personal financial statement is an important tool in financial planning because it will help us know our true financial status, make us able to assess the current financial situation and the possible future. It also helps us make financial decisions more effectively.

Personal financial statements: Do we need to hire an accountant?

It’s not necessary at all. We can do it ourselves. Personal financial statements are not as difficult as we think. Anyone who has no background in finance or does not have to graduate in accounting and finance can learn and do it.

But the important thing is that we should do it immediately because we will know our financial status today, what assets we have, how much debt we have, how many months or years we will have enough money to use, etc. It is better than knowing when we have a lot of debt and cannot find the money to pay, or when we are close to retirement and do not have enough money to use in our old age.

There are 3 main personal financial statements:

- Personal Balance Sheet

- Personal Income and Expense Statement

- Cash Budget

Personal Balance Sheet

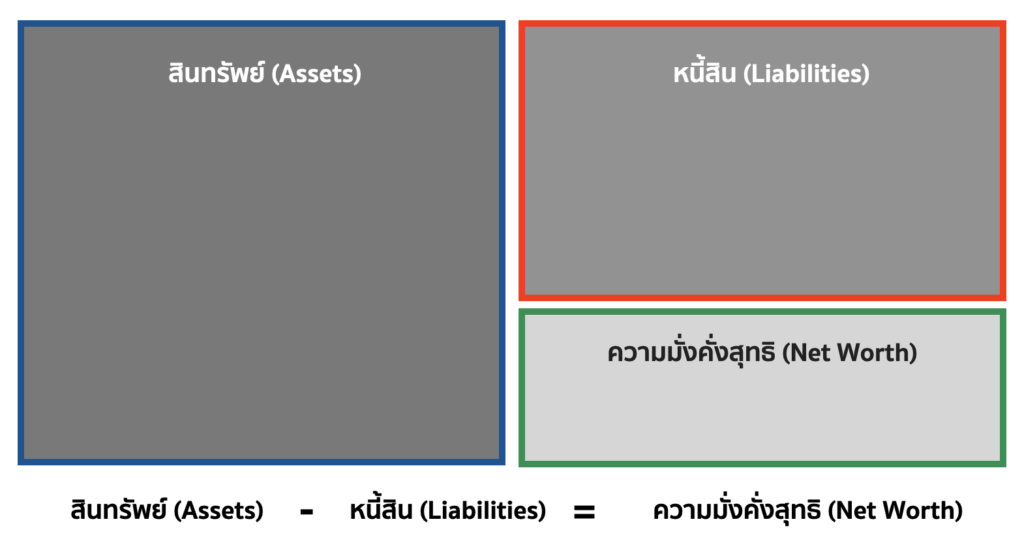

A personal balance sheet is a report that shows the financial status of a person at a given point in time. A personal balance sheet lets us know what assets we have, how much they are worth, how many liabilities we have, and finally how much net worth we have.

Personal balance sheet is an important starting point for financial planning because it helps us to accurately assess our current financial wealth, making it easier to set goals and plan finances appropriately according to our needs.

“Personal Balance Sheet: Assets – Liabilities = Net Wealth”

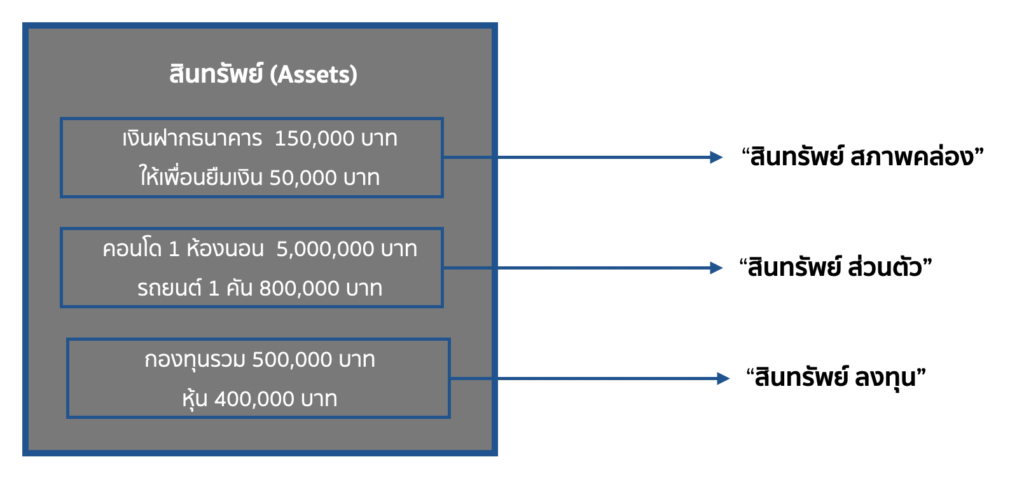

Assets are a list of various properties that we own. There are many types of assets, different in nature and utility. Assets are divided into:

- Liquid assets (e.g. cash, bank deposits, short-term investments, etc.)

- Personal assets (such as houses, cars, appliances, jewelry, etc.) and

- Investment assets (e.g. mutual funds, bonds, stocks, gold, real estate, land, etc.)

Recording the price of assets, especially assets with fluctuating prices such as land and cars, look at the market price in the year that we prepare the personal balance sheet. For example, a car was bought with cash 2 years ago for 850,000 baht. The value of this car at this time must refer to the current trading price, for example, in the market it is traded at 350,000 baht, etc. We take this value and put it on the asset side as the value of our car.

Or in the case of land that was bought as an investment 4 years ago, priced at 250,000 baht, the trading value or appraisal price this year is 600,000 baht, we must also update the value of this land in our asset list.

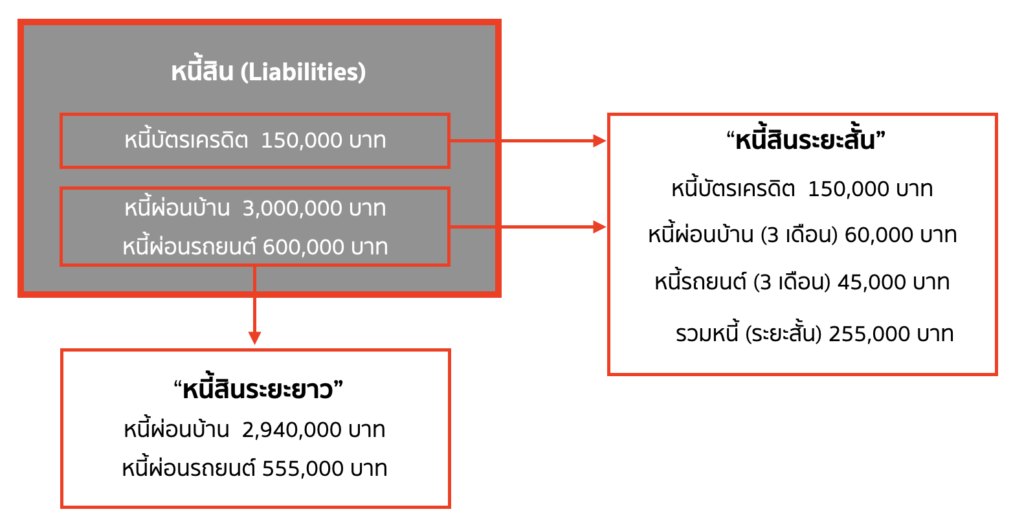

Liabilities are financial items that we have borrowed from others and have a contractual obligation to repay in the future. Liabilities may be personal debts or family debts and are divided into:

- Short-term liabilities (Current Liabilities: Current liabilities that must be paid within 1 year, such as credit card debt or other installment payments, both with interest and 0% interest) and

- Long-term Liabilities (Long-term Liabilities: Debts with a repayment period of more than 1 year, such as debt from home loans, car loans, etc.)

From the above example, we will have to consolidate the home loan and car loan into short-term debt. Consider it for 3 months. The reason for considering it is because it is a regular debt that must be paid within a 2-3 month timeframe. If we need to plan for emergency funds, we will have to include this group of installments as well.

Net worth is the remaining amount of our assets after deducting all of our debts. This remaining amount is our real assets and is a representation of our wealth.

“Assets – Liabilities = Net Wealth”

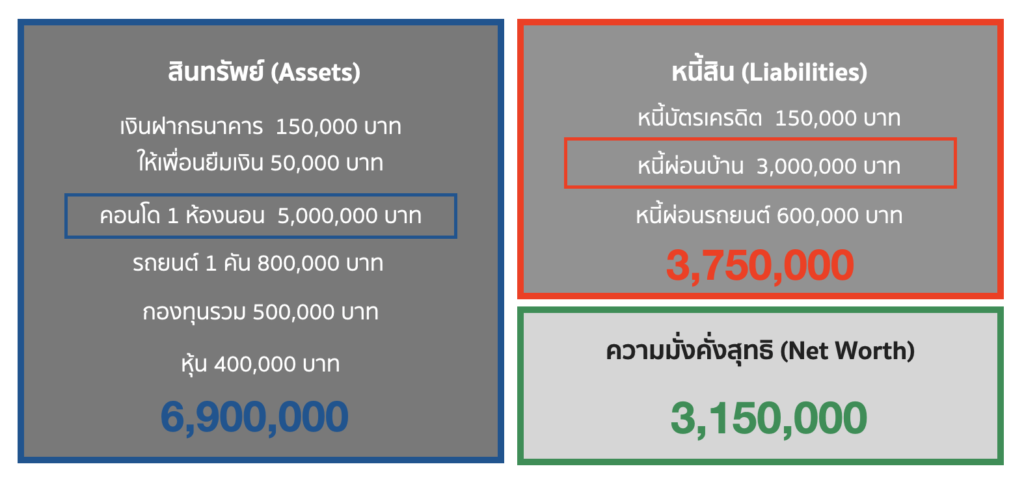

For houses or condos, we give the latest appraisal price. For example, we bought a condo a while ago and the current appraisal price is 5 million baht (put it in the personal assets side). We have already paid off the installments and the remaining debt today is 3 million baht (put it in the long-term debt side). If we only consider this condo, the remaining assets we have are 5 – 3 = 2 million baht.

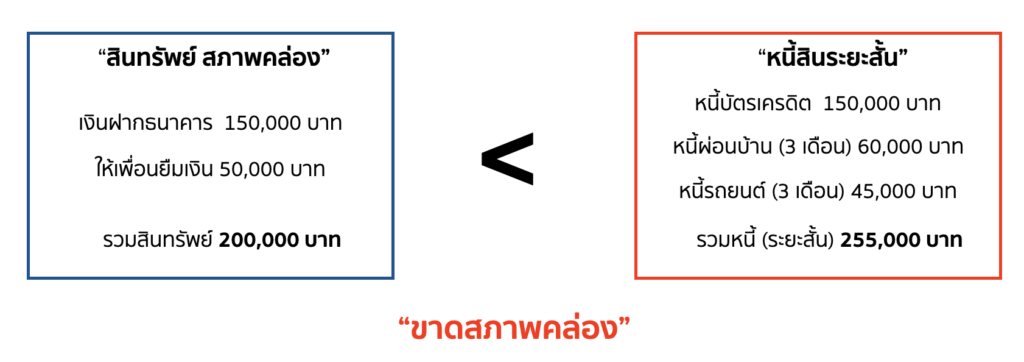

“But the problem that most working people are facing is the lack of financial liquidity.”

If at any time our “liquid assets” and “short-term debts” are less than short-term debts, it means that we are lacking financial liquidity and there is a high chance that we will have to borrow money to pay off short-term debts, like many people do, which is to use cash cards to pay off credit card debts, causing the more we pay off debts, the more debts we have, and it becomes a cycle of huge debts.

Solution: If you are already in heavy debt, you can do this by converting “short-term debt” into “long-term debt” by applying for a long-term loan with lower interest rates to pay off credit card debt with higher interest rates.

That’s why he recommends that working people have some emergency reserves, such as at least 3-6 times of their monthly expenses, in case of an emergency situation, such as sudden unemployment or temporary inability to work. At the very least, having this reserve can help pay off our debts during times of trouble.

So, if we just fill out a simple form for our personal balance sheet, we will immediately know how financially risky or safe our current situation is.

Personal Income and Expense Statement

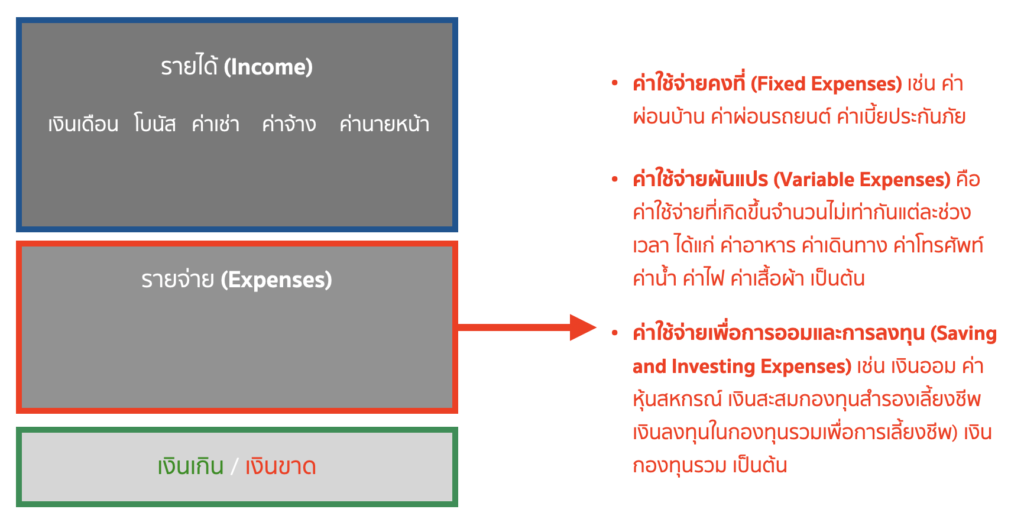

A personal income and expense statement is a summary report of an individual’s income and expenses that occurred over a period of time, such as 1 week, 1 month, or 1 year.

Personal income and expense statements clearly reflect our spending behavior, which is very important basic information for improving financial behavior and planning spending for the future.

Our habits and spending behaviors will determine whether our financial future will survive or fall. Let’s understand what the personal income and expense budget consists of.

“Income – Expenses = Surplus or Remaining Income”

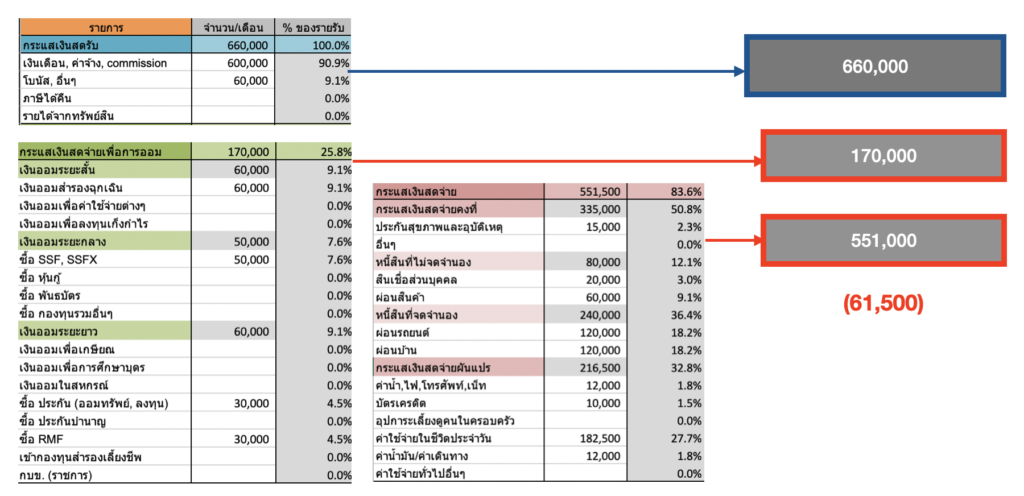

This shows the problem of Cash Flow or cash flow because from the income and expenses statement of this person in 1 year, there is a proportion of fixed expenses and variable expenses as high as 83.6% of income and also the cost of saving and investment is as high as 25.8%. The higher the savings and investment, the better. But if it causes a problem in Cash Flow, we have to consider where we can reduce it. If we manage spending behavior and help reduce fixed expenses and variable expenses to no more than 70%, it will be good and will leave more money. This is another example of how to solve the problem of Cash flow.

He suggested that at least we should have a savings and investment ratio of at least 10% of our income.

To achieve this, we need to reduce both fixed and variable expenses.

Cash Budget

A cash budget is a plan that shows the total amount of cash that is expected to be generated on a weekly or monthly basis. A cash budget is a simple tool that helps us control our spending in advance. If we have extra cash, we can plan for savings and investments. If we don’t have enough cash, we can prepare to cut expenses or find solutions.

“Personal cash budget: Expected cash receipts – Cash payments = Surplus/shortage”

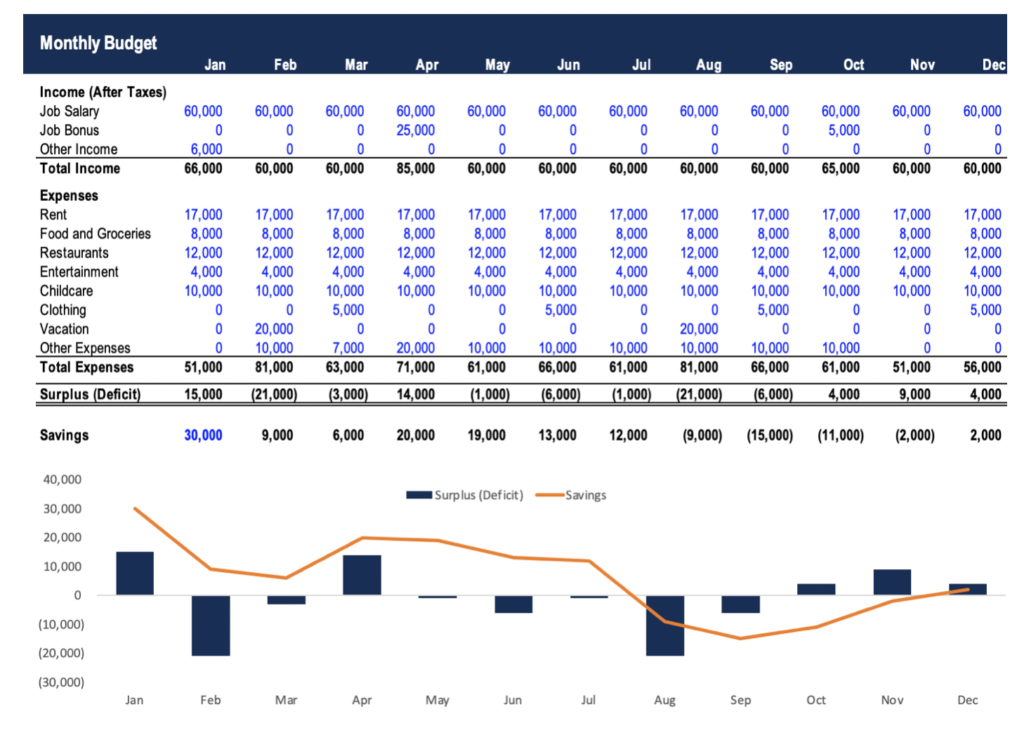

Making a cash budget will show us what our cash situation will be like at the end of the fiscal year. For example, in Figure 8, at the beginning of the year, we had 30,000 baht in savings. If we plan to estimate expenses according to this table (income as salary plus bonus), we will find that at the end of the year, we will have only 2,000 baht left in cash. The reason is due to spending behavior.

But he is still lucky because this is a plan. When the plan doesn’t turn out well, he still has a chance to adjust his behavior or spending habits. But on the other hand, if he doesn’t have a plan, doesn’t make a plan, or doesn’t know what his current financial situation is, it will definitely be difficult for him to be successful in both work and money.

Conclusion for this story

“People who understand finances well, plus have proper financial discipline, no matter what career they pursue, can achieve success.”

Because personal financial statements help us plan our finances and our family’s finances correctly, promote us to realize the importance of spending correctly in every aspect of life, and also serve as a good financial foundation for those who are interested in becoming entrepreneurs in the future.

Source:

For more articles on personal financial management, please visit:

Personal financial management is a very important skill, but it is not taught in schools.